Text|Intelligent Relativity

Author|Kinki

Recently, Hunan Yuneng, a leader in lithium iron phosphate cathode materials, officially landed on the A-share market. On the day of listing, the market value exceeded 40 billion yuan, and investors can earn 14,900 yuan if they win a lottery. However, after the "good start", Hunan Yuneng's stock price has fallen all the way, and its market value has dropped to about 35.6 billion yuan as of the date of writing.

Hunan Yuneng, which took advantage of the new energy development Dongfeng to go public, can be said to have taken advantage of the right time, place and people. The revenue and net profit attributable to the mother have increased from 162 million yuan and 11.71 million yuan in 2018 to 7.03 billion yuan and 2021 respectively. 1.175 billion yuan, and the profit soared nearly 97 times. No wonder the winners are crazy about it.

But for investors, it is more important to stand in the present and look at the future. For Hunan Yuneng, the revenue and profit have soared more than 70 times and 90 times. How much room for growth is there? After the hustle and bustle dies down, whether Hunan Yuneng's related-party transactions, executives' "snake swallowing elephant" and other management issues will affect the future of the company, these risks attached to the water surface, I am afraid that it is worth pondering.

Take advantage of the wind, and you will have a noble life

Why can Hunan Yuneng develop crazily in just 4 years? On the one hand, under the background of "dual carbon", the new energy vehicle market is developing rapidly. In 2020, the sales volume of new energy vehicles will be 1.367 million, a year-on-year increase of 10.9%; but in 2021, its sales volume will reach 3.521 million, a year-on-year Both have increased by 1.6 times; this trend will continue in 2022, with a growth rate close to 100%.

The high prosperity of downstream new energy vehicles has led to a surge in demand for midstream lithium battery and upstream material manufacturers. This bottom-up demand transmission has caused a "big explosion" in the performance of many material manufacturers, lithium mine manufacturers, and battery manufacturers in recent years. ".

In addition to benefiting from the high prosperity of the new energy industry, the installed capacity of lithium iron phosphate has gradually surpassed that of ternary materials in recent years, which is another bonus that the industry has given to Hunan Yuneng.

According to different chemical compositions, positive electrode materials can be divided into: ternary materials, lithium iron phosphate, lithium cobalt oxide and lithium manganese oxide. Among them, ternary materials are mainly used in power lithium batteries, and lithium iron phosphate is used in both power lithium batteries and energy storage fields.

Before 2021, ternary materials have always been the mainstream materials for lithium batteries, but starting from 2021, this trend has reversed. In the long run, it is unlikely that ternary materials can be reversed.

There are several main reasons. First, the price of nickel and cobalt elements in ternary materials is very high, resulting in the cost of ternary materials being much higher than that of lithium iron phosphate. Therefore, most downstream OEMs prefer to choose more cost-effective battery materials, and the industry has also begun to work together to improve the product power of lithium iron phosphate batteries.

Since BYD launched the lithium iron phosphate blade battery in 2020, its "traditional disadvantage" that its energy density is lower than that of the ternary lithium battery has weakened, and it can basically meet the needs of all models with a battery life of less than 600 kilometers.

Secondly, last year, relevant departments put forward a clear requirement to prohibit the use of ternary lithium batteries and sodium-sulfur batteries for electrochemical energy storage power stations. Considering safety considerations, in the long run, lithium iron phosphate and sodium ions are more suitable for energy storage batteries .

Under the multiple benefits, battery factories and lithium mining factories in the middle and upper reaches are even more popular than new energy vehicles. Some car companies once complained in public, saying that due to the high price of batteries, car companies are tantamount to working for Ningde era. However, Ningde Times also responded quickly, saying that it was also struggling on the verge of profitability, implying that King Ning was also working for a lithium mine.

Because of the uniqueness of resources, mines do hold the lifeblood of downstream manufacturers, but from another perspective, it is precisely because downstream cars and batteries can create brands and market demand that the price of lithium mines soars. From this point of view, the "hurricane" of the new energy industry will benefit the entire industrial chain, but if there are no battery factories and vehicle manufacturers to be responsible for "playing the vanguard", the upstream industry chain will not be able to make money alone.

As a "resource porter", Hunan Yuneng is well aware of this truth, so he embraced the thighs of the battery factory Ningde Times and the automaker BYD early on. The little brother in the industry turned around and became the boss of the industry.

In 2018, the industry leader was actually Defang Nano. At that time, its revenue had reached 1.054 billion yuan, while Hunan Yuneng had only 162 million yuan. However, in 2020, Ningde Times and BYD both participated in the last round of financing before Hunan Yuneng’s listing. After becoming their own family, Hunan Yuneng’s development will be more stable, and its revenue exceeded that of Defang Nano in that year. .

From the perspective of revenue ratio, Ningde Times and BYD's contribution to Hunan Yuneng's revenue has remained at around 90% for a long time. From the perspective of business model, there is indeed a risk of too single customer.

But from the perspective of market development, leading companies such as Ningde Times and BYD will not only choose one upstream cooperative enterprise. For example, Yichun Times, a wholly-owned subsidiary of Ningde Times, has a 30,000-ton joint venture with Tangshan Xinfeng Lithium Industry For the cooperation project of lithium carbonate, Hunan Yuneng is just one of the partners in Ningde era to balance the upstream price.

For the Ningde era, as long as the cost, risk and quality are controllable, and the cooperative company is still "in-house", in the absence of major equity changes, it is extremely unlikely that the Ningde era will voluntarily cancel the order.

"Xiangtan Department" executives are thought-provoking

Therefore, the risk point of related party transactions is a plus item for Hunan Yuneng, not a minus item. Compared with this, the affiliated acquisition of Hunan Yuneng's executive team is even more thought-provoking.

When it comes to Hunan Yuneng, we have to mention another listed company, Xiangtan Electrochemical. As the incubator of Hunan Yuneng, most of Hunan Yuneng's executive team comes from Xiangtan Electrochemical. Hunan Yuneng's board of directors has 9 members, all of whom are from Denka Group and its related parties, including 3 independent directors, and a total of 5 directors are from Xiangtan University.

At present, due to the relatively dispersed shareholding structure of Hunan Yuneng, the company has no controlling shareholder or actual controller. Therefore, compared with other listed companies, Hunan Yuneng's board of directors has greater voice and control power, and the background of "Xiangtan Department" also makes Hunan Yuneng's board of directors unprecedentedly harmonious.

But this "harmony" may not necessarily be a good thing for the company's future development. At present, the state of Hunan Yuneng without an actual controller may bring certain potential risks to the company, such as the loss of market opportunities and the use of raised funds due to the decline in decision-making efficiency.

Therefore, the board of directors will most likely take on the function of leading the company's development, but will this increase the difficulty of supervising the company's internal management? Will the "Xiangtan Department" be a bit "too powerful"?

At present, the relevant executives of the "Xiangtan Department" have staged a "snake swallowing elephant" acquisition before Hunan Yuneng's listing.

According to the prospectus of Hunan Yuneng, the company acquired its subsidiary Guangxi Yuning in December 2020, generating 180 million goodwill. But at the time of the acquisition, Guangxi Yuning's net assets were only more than 30 million yuan. How was the nearly 6 times premium calculated? Can Guangxi Yuning really bring such a huge potential return to Hunan Yuneng?

But if we look at the equity portfolio of Guangxi Yuning, all this seems to make sense again. Before the acquisition, the main managers of Guangxi Yuning were Luo Ze, Zhou Shouhong, and Tan Xinqiao. Tan Xinqiao was the chairman of Hunan Yuneng, and Zhou Shouhong was the deputy general manager. This is already a typical related acquisition.

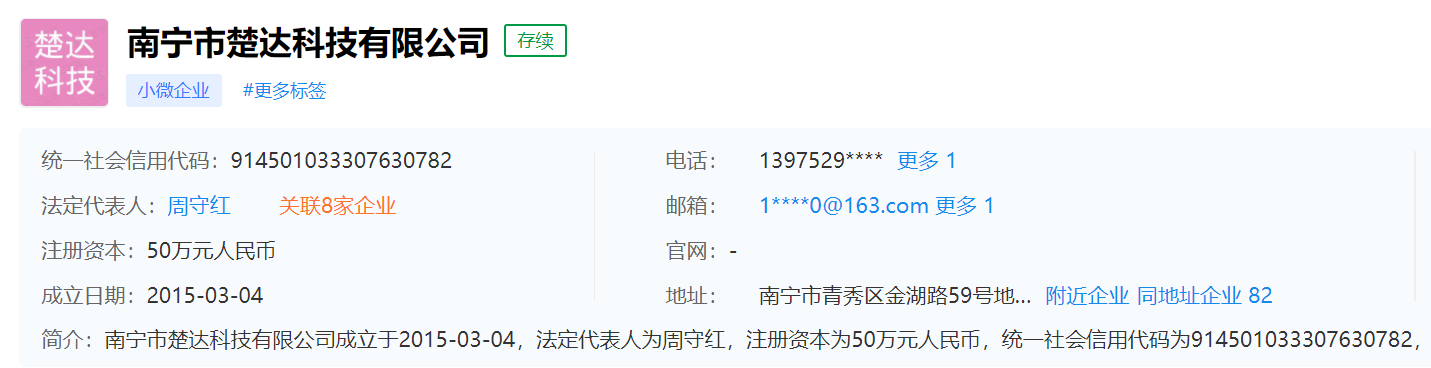

What is even more surprising is that Nanning Chuda Technology Co., Ltd., one of the original shareholders of Guangxi Yuning, has a registered capital of only 500,000 yuan, and Zhou Shouhong holds 70% of the shares. It can be said that a series of shareholders such as Zhou Shouhong obtained 30% of the shares of Guangxi Yuning when it was acquired with only 500,000 yuan, with a premium of more than 60 million yuan, which is a typical "snake swallowing elephant".

除此之外,南宁市楚达科技有限公司拿着从广西裕宁那得来的投资收益,转手又投了裕能新能源,占股3.95%,按当下湖南裕能350亿元左右的市值来算,这点股份可值差不多14亿元了呀,堪称资本魔法。

众所周知,湖南裕能的大股东是电化集团,属于湘潭市国资委下属企业,目前并不确定以上这些关联交易是否都已被其知悉,如果没有的话,当中又是否存在国有资产流失之嫌?

产能会否成为达摩利斯之剑

除了内部管理问题之外,对整个新能源行业而言,产能也是悬在头上的“达摩利斯之剑”。

这几年由于下游新能源车市场的加速发展,推动了上游原材料的需求量上涨,但这些高纯度、电池级别的金属原材料开采和提炼的难度大、周期长,导致其产出远远跟不上需求。

不过,新能源行业的“供需错配”也在逐渐调整过来,比如不少金属材料的供应量已在提高,再叠加下游产业链库存累积、新能源车增长放缓等因素影响,东吴证券曾预测,2023年全国磷酸铁锂整体供给量将达到237.1万吨。但是需求量仅为184.6万吨。

那么,湖南裕能会否遭遇“产能过剩”危机?先看供给,这两年上游矿厂、材料厂无疑都处于扩张阶段,据GGII不完全统计,2022年中国锂电四大主材规划投资金额超5000亿元,扩产项目数量为156个。

两大行业龙头包括湖南裕能和德方纳米都在加速扩产,比如湖南裕能就在招股书中提到,此次募集资金将用于四川裕能三期年产6万吨磷酸铁锂项目、四川裕能四期年产6万吨磷酸铁锂项目。

东吴证券预测,湖南裕能在2022年底能实现40万吨产能,并在2023年底实现89.3万吨产能。如果机构的预测数据准确,两年后光湖南裕能一家企业就能满足全球一半的磷酸铁锂需求,产能过剩危机确实存在。

但我们再看需求。或许在几年之后,新能源材料的产能真的会“过剩”,但随着技术发展和行业变化,除去新能源车以外,光伏、风电等行业仍处于发展的早期阶段,市场会否爆发出新的需求,目前也难下定论。

再者,产能过剩并不等于产量过剩,在数字化时代,矿厂和材料厂都会根据实际需求调整产出,基本不存在盲目生产导致产量过剩的问题。

在行业仍处于高速发展阶段时,盲目刹停扩产显然也并不明智,但企业确实也应该将“产能忧虑”摆在面前。面对可能存在的产能过剩问题,技术迭代是关键。

比如竞争对手德方纳米已开始探索磷酸锰铁锂技术路线,相较于磷酸铁锂,磷酸锰铁锂的能量密度可以提升10%以上,有望提高续航里程以及缩短充电时间。

目前,德方纳米年产11万吨磷酸锰铁锂项目已经投产,而湖南裕能还在研发磷酸锰铁锂的过程中,尚未批量生产。不过,湖南裕能也并非毫无准备,其在投资者互动平台中也曾表示,会积极关注新技术路线,同时保持产品竞争力。

总的来说,湖南裕能近年的“狂飙式”发展,既有行业红利,也有贵人红利,但作为国企关联企业,其崛起当然也离不开政府背书。

但正是因为这一层关系,一方面能让投资者对其实力感到更安心,但另一方面,却要提防背后这些错综复杂的关联人物、事件,避免其会影响公司未来的发展,这样企业才能走得更远、更稳,才能更好向一众中小股东交代。

*本文图片均来源于网络

此内容为【智能相对论】原创,

仅代表个人观点,未经授权,任何人不得以任何方式使用,包括转载、摘编、复制或建立镜像。

部分图片来自网络,且未核实版权归属,不作为商业用途,如有侵犯,请作者与我们联系。

•AI产业新媒体;

•澎湃新闻科技榜单月度top5;

•文章长期“霸占”钛媒体热门文章排行榜TOP10;

•著有《人工智能 十万个为什么》

•【重点关注领域】智能家电(含白电、黑电、智能手机、无人机等AIoT设备)、智能驾驶、AI+医疗、机器人、物联网、AI+金融、AI+教育、AR/VR、云计算、开发者以及背后的芯片、算法等。