In the past few years of working in the banking technology department, I have frequently heard the concept of "open banking".

The term "open banking" refers to a business model in which financial data is shared between parties, including financial service providers (banks, insurance companies, retailers, etc.), between providers and customers, through application programming interfaces (APIs). data shared between individuals, or between individuals. It does not refer to a certain technology or solution, but a new way to provide customers with more choices of products and services. For banks that have traditionally employed non-digital processes, some centuries old, this new approach is undoubtedly disruptive to the bank's business model.

Why is Open Banking important?

The needs of users keep pace with the times. With the advancement of Web 2.0 to 3.0, all aspects of users' lives are beginning to tend to be digitized. At the same time, users also hope that financial service providers can provide better solutions. Banks' traditional business models have become increasingly irrelevant in today's digital environment. Open Banking helps simplify digital transactions, enhances the security of financial data online, and has the potential to change the way people interact with financial institutions.

Open banking (also known as connected banking) is already widely used in many countries, where banks and other companies collaborate to develop new products and services, such as using digital means or e-wallets to purchase goods. In today's digital economy, consumers demand better products and services from financial institutions. Many banks are embracing this new model with enthusiasm.

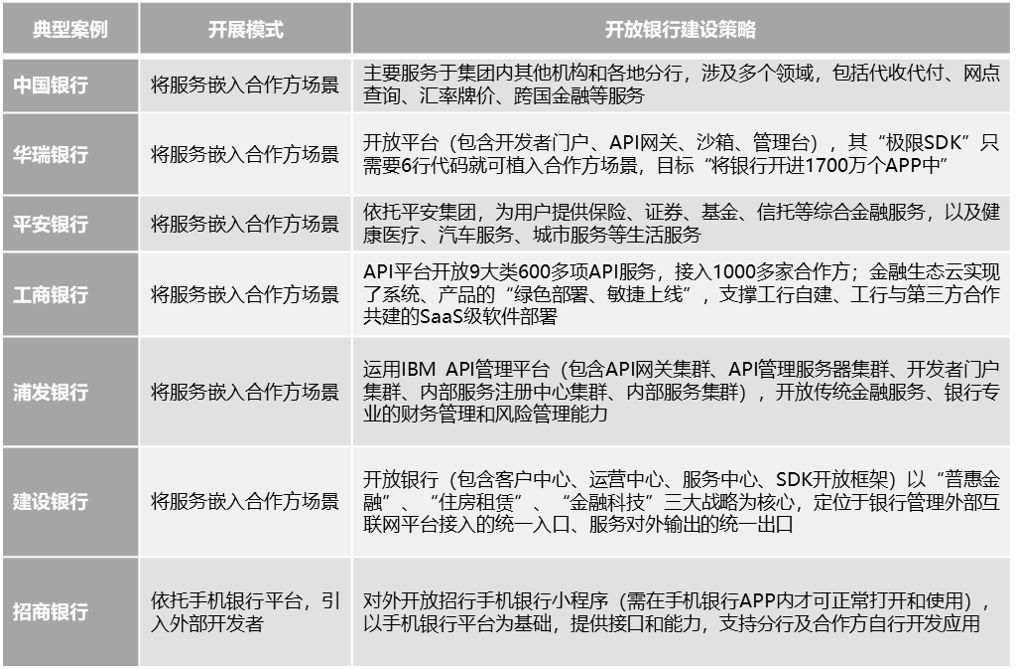

The concept of open banking in China started relatively late. It is generally believed that the first open bank established in my country is the API unbounded open bank of Shanghai Pudong Development Bank. The bank lays out its business entirely with the concept of open banking. At the same time, its development strategy for its first-class digital ecological bank is the concept of open banking, embedding the development of financial technology into the development framework of open banking. Later, around 2018, after the concept of "open banking" emerged, banks introduced it into their own financial technology development strategies and plans.

The booming development of small program ecology and technology

Let’s talk about the mini-program ecology first: since the WeChat mini-program was officially launched in 2017, it has quickly become an important ecosystem in China’s mobile Internet industry. As of the end of 2021, the monthly active users of WeChat Mini Programs have exceeded 120 million, covering various industry application scenarios such as e-commerce, finance, medical care, education, tourism, and travel. The WeChat mini-program ecosystem is also constantly improving, providing developers with a wealth of development tools, templates, and open source components and other resources.

Let’s talk about small program technology: Compared with traditional native application development technology, small program technology has the advantages of light weight, rapid development, cross-platform, no installation, and more user-friendly. Mini programs can be used without downloading and installing by users. At the same time, the development cost of mini programs is relatively lower, the development speed is faster, and it is easier to maintain and update. The applet technology also supports cross-platform operation and can run on multiple mobile devices at the same time, which greatly expands the coverage of applications and brings greater commercial value to enterprises and developers. Some of the more well-known small program container technology products on the market include: WeChat, Alipay, Baidu, Douyin small programs, etc., all of which are based on the technology base to improve the small program ecology of the big social platform, and can provide third parties for privatization deployment There are: FinClip , mPaaS and other products. It is understood that the small program container technology independently developed by FinClip can enable enterprises’ apps to have the ability to quickly run small programs, and their SDK can also be embedded in functional device terminals other than apps (such as Linux, Windows, MacOS, Kirin and other operating systems).

"Small program", an innovative hybrid App development model

As early as the beginning of the development of Web 2.0, the Internet industry with the most cutting-edge technology application proposed the "Native + H5" app hybrid development model, and the emergence of small program container technology can enable enterprise apps to have the ability to run small programs , forming an innovative App development model of "Native + Mini Program". Its advantages are also very obvious:

-

Cross-platform capability: a set of small program codes can run on both iOS and Android (even on a variety of terminals other than mobile phones, including Linux, Windows, MacOS, Kirin and other operating systems);

-

Experience far beyond H5 (support local cache, Webview, rich components and support library);

-

Can obtain more system permissions and complete richer product designs;

-

DOM leaks can be avoided;

-

Packet size is effectively reduced, saving traffic and storage

-

Support hot update, so that the service is no longer restricted by the release version

One of the Open Banking Trends: Super App

A Super App is a mobile application that integrates multiple functions and services, providing a wide range of services and experiences on one platform. Super Apps usually have a large number of user groups and a highly active user community. By providing convenient and diversified functions, they attract users to complete multiple tasks and meet multiple needs in one application.

Compared with traditional single-function applications, Super Apps are characterized by their diversity and comprehensiveness. Super Apps not only provide core functions, such as social networking, payment, or travel, but may also integrate other services, such as e-commerce, food delivery, and finance. This integration allows users to complete multiple operations in one application without switching between different applications.

The business value of super apps to the global economy is enormous.

First, it promotes market innovation and competition promotion. Super App provides a more comprehensive, convenient and integrated user experience by integrating multiple industries and services. They drive innovation and competition in the market by introducing innovative business models and technological solutions. Second, it provides employment and entrepreneurial opportunities. The development of super apps has created a large number of employment and entrepreneurial opportunities for the economy. They not only require a large number of technical development and operation talents, but also promote the development of related industries, such as travel, catering, logistics, etc. At the same time, it also optimizes the supply chain and logistics to a certain extent. Super App optimizes supply chain and logistics management through digitization and data-driven in various industries. They provide more efficient distribution and delivery services, reduce operating costs and time, and increase efficiency and customer satisfaction.

The development of mini-program application scene ecology benefits from the development of open source technology and responds to the actual business needs of rapid development. Some cross-terminal frameworks such as: Electron, wxPython, FinClip, Tauri, Flutter, etc. are also developing very rapidly. The terminal technology framework can not only meet the flexible technical construction of its own super app, quickly introduce third-party ecology, but also connect all connectable applications through small program container technology.