文章目录

这是一个kaggle上关于信用行为评分卡的项目,下面是我对该项目的分析过程

项目地址:https://www.kaggle.com/c/GiveMeSomeCredit/overview

数据地址:https://www.kaggle.com/c/GiveMeSomeCredit/data

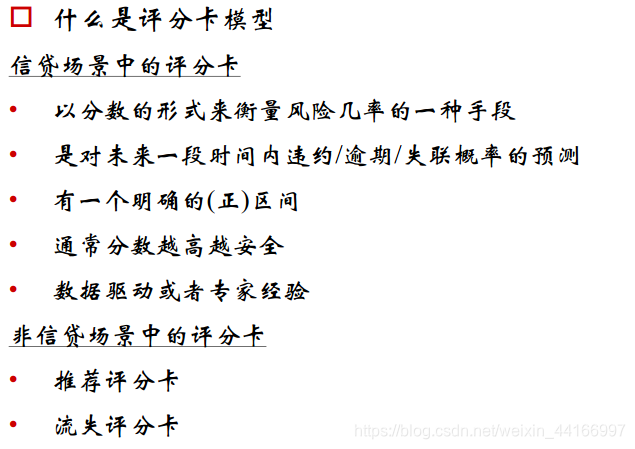

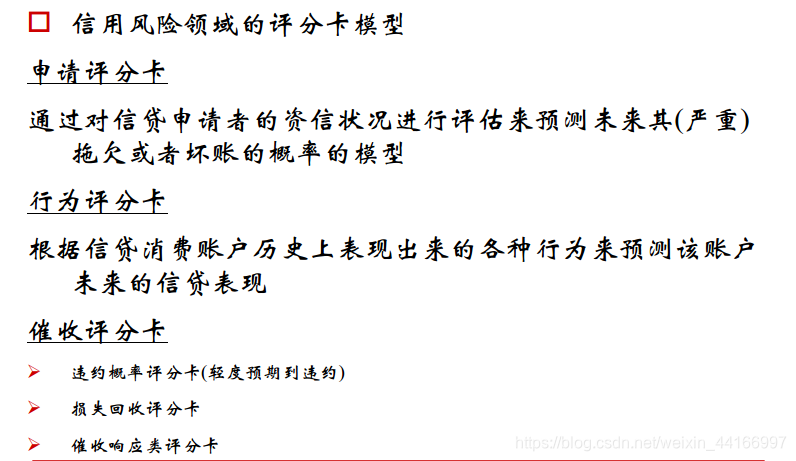

1·首先对评分卡模型的定义如下

2·在kaggle上的项目说明文档如下表

数据分析流程:

1,数据获取

2,数据预处理(空值,异常值处理)

3,对数据进行分箱,woe编码,建模预估

4,评估模型的区分能力、预测能力、稳定性,并形成模型评估报告

5,将Logistic模型转换为标准评分

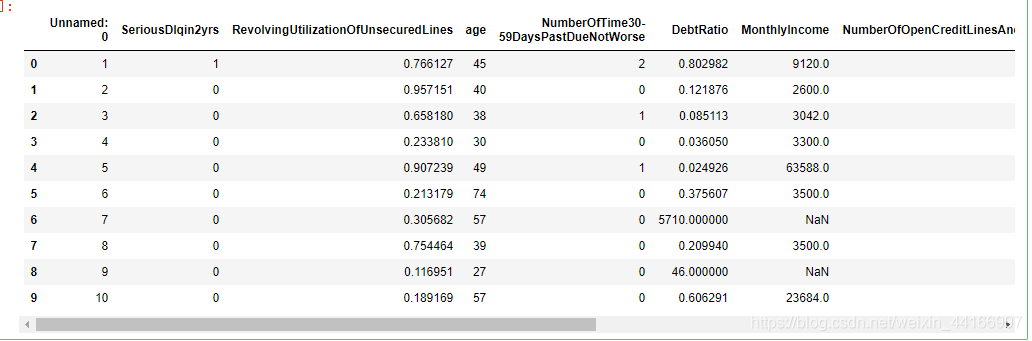

#读取数据

data = pd.read_csv(‘cs-training.csv’)

data.head(10)

#读取数据

data = pd.read_csv('cs-training.csv')

data.head(10)

#删除与索引重复的Unnamed: 0列

data = data.drop('Unnamed: 0',axis=1)

data.head(10)

states={'SeriousDlqin2yrs':'好坏客户',

'RevolvingUtilizationOfUnsecuredLines':'可用额度比值',

'age':'年龄',

'NumberOfTime30-59DaysPastDueNotWorse':'逾期30-59天笔数',

'DebtRatio':'负债率',

'MonthlyIncome':'月收入',

'NumberOfOpenCreditLinesAndLoans':'信贷数量',

'NumberOfTimes90DaysLate':'逾期90天笔数',

'NumberRealEstateLoansOrLines':'固定资产贷款量',

'NumberOfTime60-89DaysPastDueNotWorse':'逾期60-89天笔数',

'NumberOfDependents':'家属数量'}

data.rename(columns=states,inplace=True)

data.head() #修改英文字段名为中文字段名

注意:这里 坏客户是1,好客户对应0,

一,数据预处理

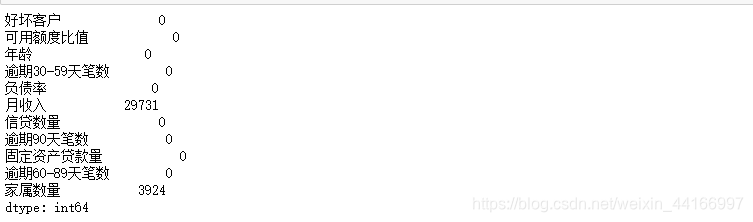

1,缺失值处理

#查看空值数量

data.isnull().sum()

#方法一缺失值处理

# 比较MonthlyIncome的中位数,平均数,众数,由于众数与中位数比较相近,故选择中位数作为空值填充值

# 对于NumberOfDependents ,因为缺失数据比例较少,所以直接舍弃这些数据

data1 = data.fillna({'月收入':5400})

data1=data1.dropna()

data1.head(10)

# 方法二通过随机森林填充空缺值

from sklearn.ensemble import RandomForestRegressor

# 定义方法

def set_missing(data):

# 这里是对 '月收入' 这列的空值进行填充,故取值时不使用 '家属数量' 列的数据(因为有空缺值)

# 把已有的数值型特征取出来

process_data = data.iloc[:,[5,0,1,2,3,4,6,7,8,9]]

# 分成已知该特征和未知该特征两部分

known = process_data[process_data['月收入'].notnull()].values

unknown = process_data[process_data['月收入'].isnull()].values

# X为特征属性值

x = known[:, 1:]

# y为结果标签值

y = known[:, 0]

# fit到RandomForestRegressor之中

rfr = RandomForestRegressor(random_state=0, n_estimators=200,max_depth=3,n_jobs=-1)

rfr.fit(x,y)

# 用得到的模型进行未知特征值预测

predicted = rfr.predict(unknown[:, 1:]).round(0)

print(predicted)

# 用得到的预测结果填补原缺失数据

data.loc[(data['月收入'].isnull()), '月收入'] = predicted

#对于 '家属数量' ,因为缺失数据比例较少,所以直接直接舍弃这些数据

data=data.dropna()

return data

data2 = data.copy()

data2 = set_missing(data2)

data2.head(10)

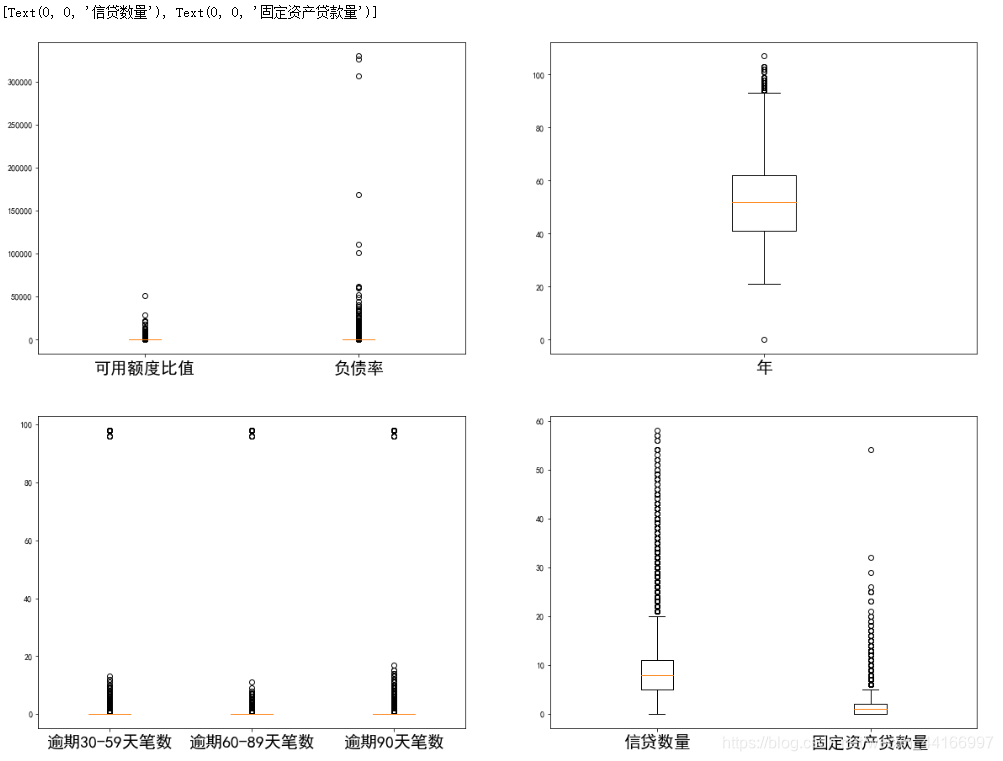

2,异常值处理

from pylab import mpl #用户设置字体

mpl.rcParams['font.sans-serif'] = ['SimHei']

x1=data2['可用额度比值']

x2=data2['负债率']

x3=data2["年龄"]

x4=data2["逾期30-59天笔数"]

x5=data2["逾期60-89天笔数"]

x6=data2["逾期90天笔数"]

x7=data2["信贷数量"]

x8=data2["固定资产贷款量"]

fig=plt.figure(figsize=(20,15))

ax1=fig.add_subplot(221)

ax2=fig.add_subplot(222)

ax3=fig.add_subplot(223)

ax4=fig.add_subplot(224)

ax1.boxplot([x1,x2])

ax1.set_xticklabels(["可用额度比值","负债率"], fontsize=20)

ax2.boxplot(x3)

ax2.set_xticklabels("年龄", fontsize=20)

ax3.boxplot([x4,x5,x6])

ax3.set_xticklabels(["逾期30-59天笔数","逾期60-89天笔数","逾期90天笔数"], fontsize=20)

ax4.boxplot([x7,x8])

ax4.set_xticklabels(["信贷数量","固定资产贷款量"], fontsize=20)

# 异常值处理消除不合逻辑的数据和超级离群的数据,可用额度比值应该小于1,年龄为0的是异常值,逾期天数笔数大于80的是超级离群数据,

# 固定资产贷款量大于50的是超级离群数据,将这些离群值过滤掉,筛选出剩余部分数据。

data2=data2[data2['可用额度比值']<1]

data2=data2[data2['年龄']>0]

data2=data2[data2['逾期30-59天笔数']<80]

data2=data2[data2['逾期60-89天笔数']<80]

data2=data2[data2['逾期90天笔数']<80]

data2=data2[data2['固定资产贷款量']<50]

data2.shape

二,变量的相关性分析

1,单变量分析

2,多变量分析

相关性分析在整个流程当中对数据的变动不大,主要起到了一种催化的作用,作为一种“启动”开展后续工作,可以更好的了解到数据之间的一些联系和变化规律。同时在多变量分析中通过相关性也可以过滤掉一部分变量。所以此处不做详细探究。

三,特征选择

对数据进行分箱

pinf = float('inf')#正无穷大

ninf = float('-inf')#负无穷大

# 连续变量离散化

cutx3 = [ninf, 0, 1, 3, 5, pinf]

cutx6 = [ninf, 1, 2, 3, 5, pinf]

cutx7 = [ninf, 0, 1, 3, 5, pinf]

cutx8 = [ninf, 0,1,2, 3, pinf]

cutx9 = [ninf, 0, 1, 3, pinf]

cutx10 = [ninf, 0, 1, 2, 3, 5, pinf]

cut3=pd.cut(data2["逾期30-59天笔数"],cutx3,labels=False)

cut6=pd.cut(data2["信贷数量"],cutx6,labels=False)

cut7=pd.cut(data2["逾期90天笔数"],cutx7,labels=False)

cut8=pd.cut(data2["固定资产贷款量"],cutx8,labels=False)

cut9=pd.cut(data2["逾期60-89天笔数"],cutx9,labels=False)

cut10=pd.cut(data2["家属数量"],cutx10,labels=False)

#对数据进行等频分箱

cut1=pd.qcut(data2["可用额度比值"],4,labels=False)

cut2=pd.qcut(data2["年龄"],8,labels=False)

cut4=pd.qcut(data2["负债率"],3,labels=False)

cut5=pd.qcut(data2["月收入"],3,labels=False)

WOE值计算

rate=data2["好坏客户"].sum()/(data2["好坏客户"].count()-data2["好坏客户"].sum())

def get_woe_data(cut):

grouped=data2["好坏客户"].groupby(cut,as_index = True).value_counts()

woe=np.log(grouped.unstack().iloc[:,1]/grouped.unstack().iloc[:,0]/rate)

return woe

cut1_woe=get_woe_data(cut1)

cut2_woe=get_woe_data(cut2)

cut3_woe=get_woe_data(cut3)

cut4_woe=get_woe_data(cut4)

cut5_woe=get_woe_data(cut5)

cut6_woe=get_woe_data(cut6)

cut7_woe=get_woe_data(cut7)

cut8_woe=get_woe_data(cut8)

cut9_woe=get_woe_data(cut9)

cut10_woe=get_woe_data(cut10)

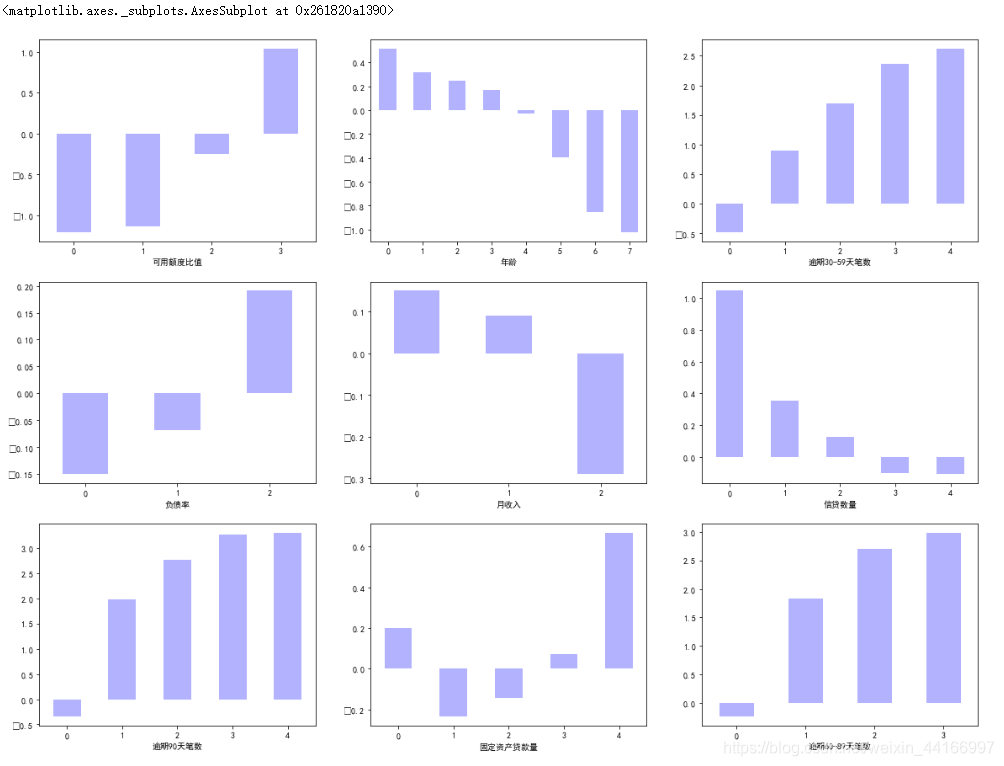

#抽选几个变量查看woe来分析分箱是否合理

fig=plt.figure(figsize=(20,15))

ax1=fig.add_subplot(331)

ax2=fig.add_subplot(332)

ax3=fig.add_subplot(333)

ax4=fig.add_subplot(334)

ax5=fig.add_subplot(335)

ax6=fig.add_subplot(336)

ax7=fig.add_subplot(337)

ax8=fig.add_subplot(338)

ax9=fig.add_subplot(339)

cut1_woe.plot.bar(ax=ax1,color='b',alpha=0.3,rot=0)

cut2_woe.plot.bar(ax=ax2,color='b',alpha=0.3,rot=0)

cut3_woe.plot.bar(ax=ax3,color='b',alpha=0.3,rot=0)

cut4_woe.plot.bar(ax=ax4,color='b',alpha=0.3,rot=0)

cut5_woe.plot.bar(ax=ax5,color='b',alpha=0.3,rot=0)

cut6_woe.plot.bar(ax=ax6,color='b',alpha=0.3,rot=0)

cut7_woe.plot.bar(ax=ax7,color='b',alpha=0.3,rot=0)

cut8_woe.plot.bar(ax=ax8,color='b',alpha=0.3,rot=0)

cut9_woe.plot.bar(ax=ax9,color='b',alpha=0.3,rot=0)

计算iv值

def get_IV_data(cut,cut_woe):

grouped=data2["好坏客户"].groupby(cut,as_index = True).value_counts()

cut_IV=((grouped.unstack().iloc[:,1]/data2["好坏客户"].sum()-grouped.unstack().iloc[:,0]/(data2["好坏客户"].count()-data2["好坏客户"].sum()))*cut_woe).sum()

return cut_IV

#计算各分组的IV值

cut1_IV=get_IV_data(cut1,cut1_woe)

cut2_IV=get_IV_data(cut2,cut2_woe)

cut3_IV=get_IV_data(cut3,cut3_woe)

cut4_IV=get_IV_data(cut4,cut4_woe)

cut5_IV=get_IV_data(cut5,cut5_woe)

cut6_IV=get_IV_data(cut6,cut6_woe)

cut7_IV=get_IV_data(cut7,cut7_woe)

cut8_IV=get_IV_data(cut8,cut8_woe)

cut9_IV=get_IV_data(cut9,cut9_woe)

cut10_IV=get_IV_data(cut10,cut10_woe)

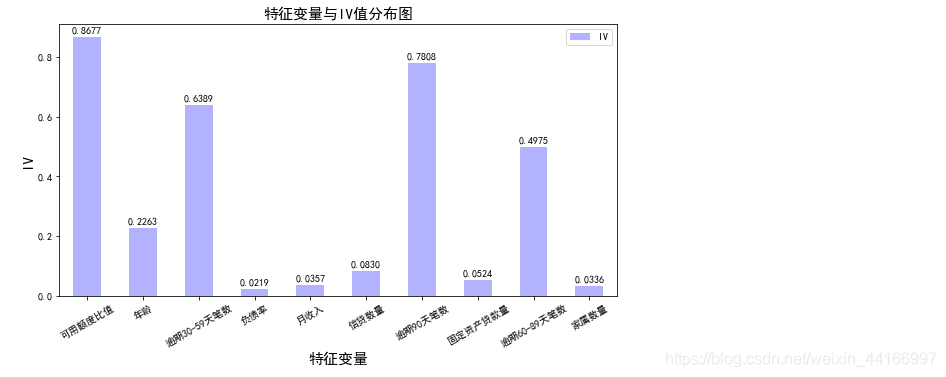

ivlist = [cut1_IV,cut2_IV,cut3_IV,cut4_IV,cut5_IV,cut6_IV,cut7_IV,cut8_IV,cut9_IV,cut10_IV]

index=['可用额度比值','年龄','逾期30-59天笔数','负债率','月收入','信贷数量','逾期90天笔数','固定资产贷款量','逾期60-89天笔数','家属数量']

IV=pd.DataFrame(ivlist,index=index,columns=['IV'])

iv=IV.plot.bar(color='b',alpha=0.3,rot=30,figsize=(10,5),fontsize=(10))

iv.set_title('特征变量与IV值分布图',fontsize=(15))

iv.set_xlabel('特征变量',fontsize=(15))

iv.set_ylabel('IV',fontsize=(15))

x = np.arange(len(index))

for a, b in zip(x, ivlist):

plt.text(a, b+0.01, '%.4f' % b, ha='center', va='bottom', fontsize=10)

WOE值替换

woe_data=pd.DataFrame() #新建df_new存放woe转换后的数据

def replace_data(cut,cut_woe):

a=[]

for i in cut.unique():

a.append(i)

a.sort()

for m in range(len(a)):

cut.replace(a[m],cut_woe.values[m],inplace=True)

return cut

woe_data["好坏客户"]=data2["好坏客户"]

woe_data["可用额度比值"]=replace_data(cut1,cut1_woe)

woe_data["年龄"]=replace_data(cut2,cut2_woe)

woe_data["逾期30-59天笔数"]=replace_data(cut3,cut3_woe)

woe_data["负债率"]=replace_data(cut4,cut4_woe)

woe_data["月收入"]=replace_data(cut5,cut5_woe)

woe_data["信贷数量"]=replace_data(cut6,cut6_woe)

woe_data["逾期90天笔数"]=replace_data(cut7,cut7_woe)

woe_data["固定资产贷款量"]=replace_data(cut8,cut8_woe)

woe_data["逾期60-89天笔数"]=replace_data(cut9,cut9_woe)

woe_data["家属数量"]=replace_data(cut10,cut10_woe)

woe_data.head()

四,进行建模训练

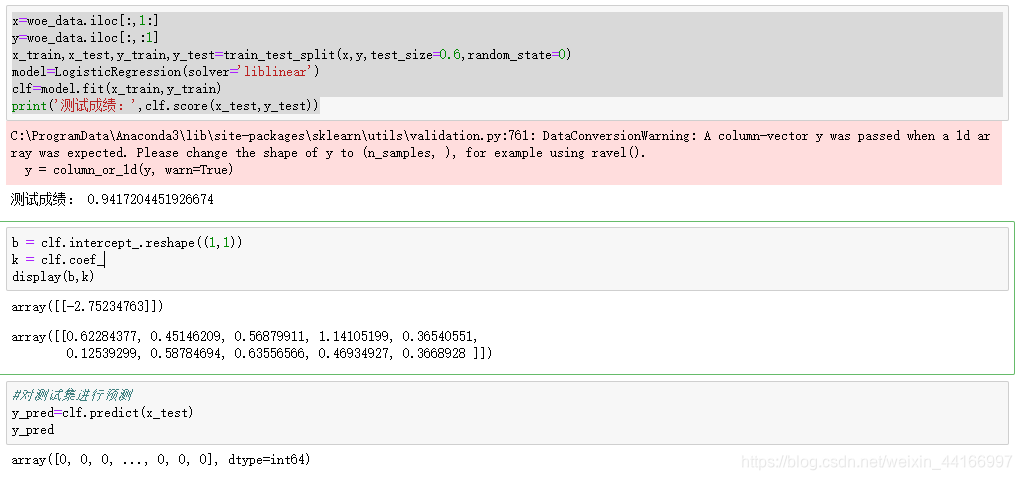

x=woe_data.iloc[:,1:]

y=woe_data.iloc[:,:1]

x_train,x_test,y_train,y_test=train_test_split(x,y,test_size=0.6,random_state=0)

model=LogisticRegression(solver='liblinear')

clf=model.fit(x_train,y_train)

print('测试成绩:',clf.score(x_test,y_test))

b = clf.intercept_.reshape((1,1))

k = clf.coef_

display(b,k)

五,模型评估

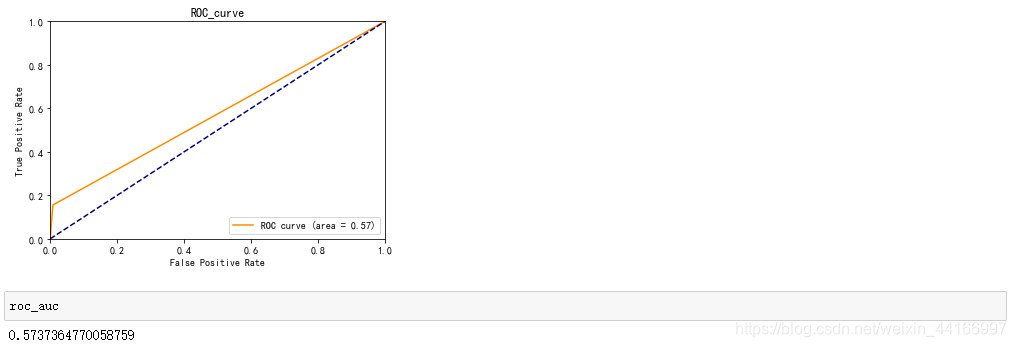

# 模型评估主要看AUC和K-S值

fpr, tpr, threshold = roc_curve(y_test, y_pred)

roc_auc = auc(fpr, tpr)

plt.plot(fpr, tpr, color='darkorange',label='ROC curve (area = %0.2f)' % roc_auc)

plt.plot([0, 1], [0, 1], color='navy', linestyle='--')

plt.xlim([0.0, 1.0])

plt.ylim([0.0, 1.0])

plt.xlabel('False Positive Rate')

plt.ylabel('True Positive Rate')

plt.title('ROC_curve')

plt.legend(loc="lower right")

plt.show()

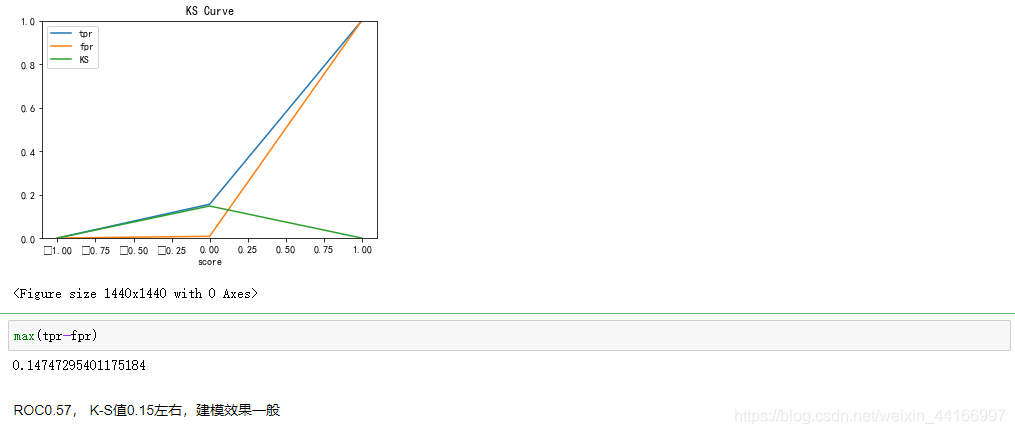

fig, ax = plt.subplots()

ax.plot(1 - threshold, tpr, label='tpr') # ks曲线要按照预测概率降序排列,所以需要1-threshold镜像

ax.plot(1 - threshold, fpr, label='fpr')

ax.plot(1 - threshold, tpr-fpr,label='KS')

plt.xlabel('score')

plt.title('KS Curve')

plt.ylim([0.0, 1.0])

plt.figure(figsize=(20,20))

legend = ax.legend(loc='upper left')

plt.show()

六,模型结果转评分

#计算各特征的得分

factor = 20 / np.log(2)

offset = 600 - 20 * np.log(20) / np.log(2)

def get_score(coe,woe,factor):

scores=[]

for w in woe:

score=round(coe*w*factor,0)

scores.append(score)

return scores

x1 = get_score(k[0][0], cut1_woe, factor)

x2 = get_score(k[0][1], cut2_woe, factor)

x3 = get_score(k[0][2], cut3_woe, factor)

x4 = get_score(k[0][3], cut4_woe, factor)

x5 = get_score(k[0][4], cut5_woe, factor)

x6 = get_score(k[0][5], cut6_woe, factor)

x7 = get_score(k[0][6], cut7_woe, factor)

x8 = get_score(k[0][7], cut8_woe, factor)

x9 = get_score(k[0][8], cut9_woe, factor)

x10 = get_score(k[0][9], cut10_woe, factor)

print("可用额度比值对应的分数:{}".format(x1))

print("年龄对应的分数:{}".format(x2))

print("逾期30-59天笔数对应的分数:{}".format(x3))

print("负债率对应的分数:{}".format(x4))

print("月收入对应的分数:{}".format(x5))

print("信贷数量对应的分数:{}".format(x6))

print("逾期90天笔数对应的分数:{}".format(x7))

print("固定资产贷款量对应的分数:{}".format(x8))

print("逾期60-89天笔数对应的分数:{}".format(x9))

print("家属数量对应的分数:{}".format(x10))

#根据变量计算分数

def compute_score(series,cut,score):

for i,j in zip(cut.values,score):

series.replace({i:j},inplace=True)

return series

ScoreDat =pd.DataFrame()

ScoreDat['x1'] = compute_score(x_test['可用额度比值'], cut1_woe, x1)

ScoreDat['x2'] = compute_score(x_test['年龄'], cut2_woe, x2)

ScoreDat['x3'] = compute_score(x_test['逾期30-59天笔数'], cut3_woe, x3)

ScoreDat['x4'] = compute_score(x_test['负债率'], cut4_woe, x4)

ScoreDat['x5'] = compute_score(x_test['月收入'], cut5_woe, x5)

ScoreDat['x6'] = compute_score(x_test['信贷数量'], cut6_woe, x6)

ScoreDat['x7'] = compute_score(x_test['逾期90天笔数'], cut7_woe, x7)

ScoreDat['x8'] = compute_score(x_test['固定资产贷款量'], cut8_woe, x8)

ScoreDat['x9'] = compute_score(x_test['逾期60-89天笔数'], cut9_woe, x9)

ScoreDat['x10'] = compute_score(x_test['家属数量'], cut10_woe, x10)

ScoreDat['Score'] = ScoreDat['x1'] + ScoreDat['x2'] + ScoreDat['x3'] +ScoreDat['x4'] +ScoreDat['x5']+ ScoreDat['x6']+ScoreDat['x7'] +ScoreDat['x8']+ ScoreDat['x9'] +ScoreDat['x10'] + 600

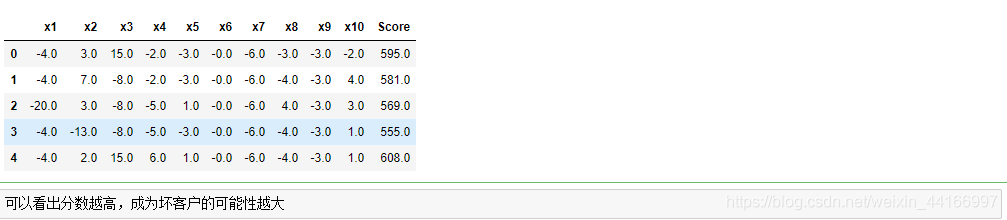

ScoreDat.head(10)

#重排索引

ScoreDat.reset_index(drop=True,inplace=True)

ScoreDat.head()